Oct 7, 2020

The coronavirus pandemic has hit consumers hard, subsequently exposing the limitations of traditional scoring in determining creditworthiness. Credit unions that can effectively leverage alternative credit data have an opportunity to not only help struggling consumers, but also expand their lending landscape.

Research reveals that traditional credit scoring measures alone are not comprehensive enough for assessing the risk of approximately 26 million creditworthy Americans who have little or no credit history. A report from Aite Group and the Consumer Financial Protection Bureau reveals that 6 in 10 U.S. adults (61%) are “credit invisibles.” These are individuals who, despite handling their financial lives responsibly and repaying loans, are either denied or are charged higher-rate premiums to cover assumptions of risk based on information that, in today’s unpredictable economic environment, may no longer be relevant.

A recent Finicity report found 95% of those affected by the pandemic are concerned about their ability to rebuild their credit or take out a loan, and 82% said they believe the current credit review process and criteria need to change to make it easier for responsible borrowers to prove their creditworthiness. Credit unions that can deliver this experience will have an edge over the competition.

Incorporating alternative data, ranging from utilities, mobile phones and rent payment history, to current income, cashflow and account balances, can provide a nuanced, more accurate picture of a person’s overall financial health. This deeper insight offers credit unions greater access to a new group of credit-eligible consumers who are often overlooked or taken advantage of. Armed with this information, credit unions will also be better positioned to anticipate consumers’ needs and offer customized loan products.

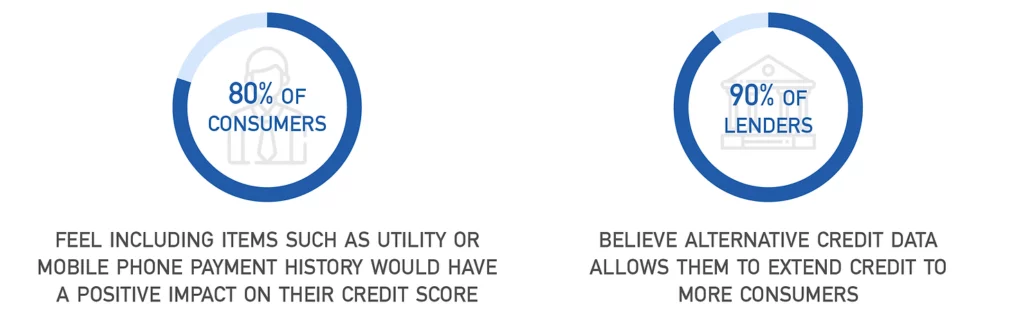

According to the Experian 2020 State of Alternative Credit Data Report, financial institutions’ use of consumer-permissioned, non-traditional data is gaining popularity. And, the overwhelming majority of consumers said they believe they should have more insight into and control over the personal financial data that’s being used to determine their creditworthiness. In addition, 3 out of 4 consumers believe they are a better borrower than their credit score represents. 80% of consumers said they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates on credit.

At Open Lending, we’ve built a platform that allows our lending partners to define the decision criteria, and then leverage our platform to make a sound lending decision in seconds on whether or not to fund the loan. This prevents embarrassingly long wait time for consumers whose credit may not be perfect and meets the demands of your indirect auto loan dealer-partners.

Consumer expectations of their financial institutions are high. Financial institutions that are able to adapt their underwriting criteria and processes to be more inclusive will have the competitive edge. By incorporating alternative credit data in assessing risk, credit unions have an opportunity to grow auto loans, build loyalty and deepen relationships with their members.

ShareAll fields required

"*" indicates required fields